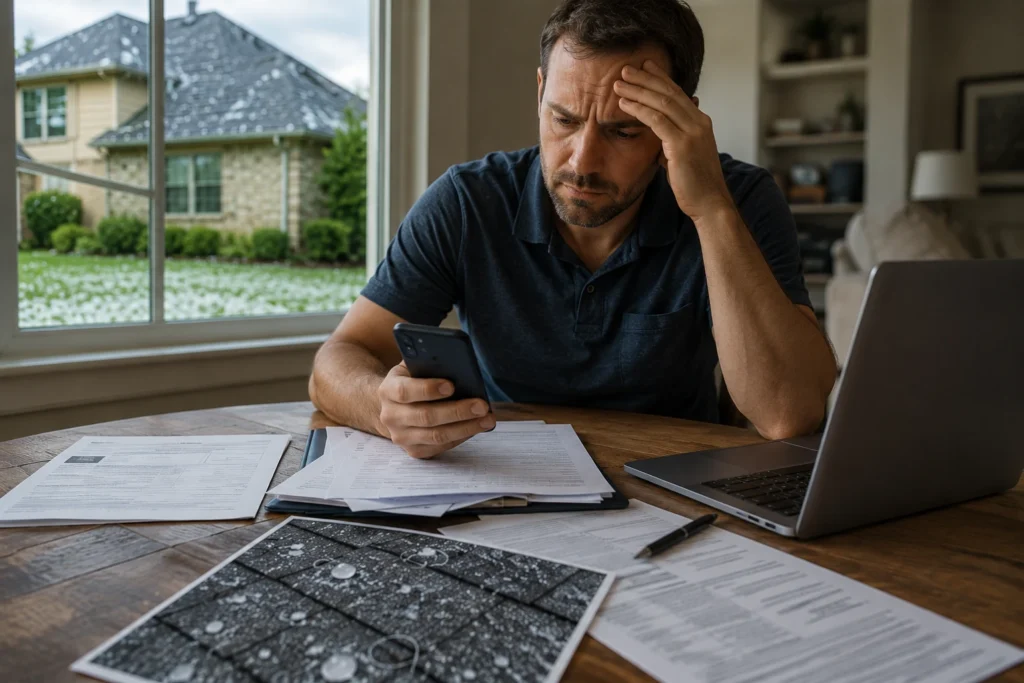

Texas hailstorms can damage a roof in minutes. Insurance claims usually take much longer. That surprises many homeowners. The hail damage claim timeline in Texas often involves inspections, documentation, negotiations, contractor scheduling, and payment reviews that can stretch over weeks or even months. One delay can slow everything down. And if mistakes happen early, the claim can become far more difficult to resolve later. Understanding the process helps homeowners move faster, avoid common problems, and protect their financial recovery after a storm.

Why Hail Damage Claims Take Time in Texas

Texas handles an enormous number of hail-related insurance claims every year. After a major storm, insurance carriers may receive thousands of claims at once. That creates immediate pressure on the system. Adjusters become overloaded. Roofing contractors fill their schedules quickly. Material shortages appear. Communication delays increase. The hail damage claim timeline in Texas becomes even longer when homeowners fail to document damage properly or wait too long to begin the process.

High Storm Volume Creates Delays

After severe storms, insurance companies often bring in catastrophe teams and independent adjusters to handle claim volume. Even then, delays remain common. Several factors affect timing:

- Number of damaged homes in the area

- Insurance carrier staffing levels

- Severity of roof damage

- Availability of contractors

- Complexity of the claim

Large metro storms can overwhelm claim systems for weeks.

Documentation Takes Time

Insurance carriers require evidence before approving major repairs or full roof replacement. That usually includes:

- Roof inspection reports

- Photos

- Contractor estimates

- Interior leak documentation

- Weather reports

The stronger the documentation becomes, the smoother the claim process usually moves.

Roof Damage Is Not Always Obvious

Some hail damage is easy to identify. Other damage remains hidden until water intrusion or deterioration begins later. Adjusters often inspect:

| Roof Area | Damage Indicators |

|---|---|

| Shingles | Bruising, cracking, granule loss |

| Gutters | Dents and impact marks |

| Flashing | Separation or punctures |

| Roof vents | Metal impacts |

| Interior ceilings | Water stains and leaks |

Disagreements over cosmetic versus functional damage can significantly extend the hail damage claim timeline in Texas.

Immediate Steps After a Hailstorm

The first few days after a storm matter more than most homeowners realize. Fast action protects both the property and the insurance claim.

Prioritize Safety

Before inspecting anything, look for immediate hazards. Watch for:

- Fallen power lines

- Structural instability

- Active leaks

- Slippery surfaces

- Broken glass

Avoid climbing onto the roof immediately after a storm. Wet roofing systems can become dangerous quickly.

Document Damage Immediately

Take photos as soon as possible. Capture:

- Roof impacts

- Dented gutters

- Damaged siding

- Broken window screens

- HVAC unit damage

- Interior water stains

Early documentation helps preserve evidence before weather exposure worsens conditions.

Schedule a Professional Roof Inspection

Professional inspections often identify damage homeowners miss entirely. That may include:

- Hidden shingle bruising

- Flashing damage

- Soft metal impacts

- Ventilation issues

- Granule displacement

Many homeowners accidentally delay the hail damage claim timeline in Texas simply because they wait too long to schedule inspections.

The Typical Hail Damage Claim Timeline in Texas

Every insurance claim is different. Still, most hail claims follow a fairly consistent pattern.

Day 1–3: Initial Inspection and Emergency Repairs

Immediately after the storm:

- Damage gets photographed

- Temporary repairs may begin

- Leaks are stabilized

- Inspection appointments are scheduled

If emergency tarping or mitigation becomes necessary, keep all invoices and receipts for reimbursement purposes.

Day 3–7: Filing the Insurance Claim

Once damage is confirmed, the claim gets reported to the insurance carrier. Homeowners usually receive:

- Claim number assignment

- Initial instructions

- Adjuster contact information

- Policy guidance

This stage moves quickly in smaller storms. During major catastrophe events, response times may slow considerably. Strong communication becomes important here. Missed calls and delayed responses often stretch the hail damage claim timeline in Texas unnecessarily.

Week 1–3: Insurance Adjuster Inspection

The insurance adjuster visits the property to inspect the damage directly. During inspections, adjusters may examine:

- Roof slopes

- Soft metal damage

- Vent impacts

- Flashing condition

- Interior water intrusion

- Gutters and siding

Roofing contractors often attend these inspections as well. That can help prevent overlooked damage from being missed entirely.

Common Inspection Problems

Several issues frequently slow claims:

- Incomplete inspections

- Weather interruptions

- Limited attic access

- Damage age disputes

- Cosmetic damage arguments

This stage often becomes one of the biggest turning points in the hail damage claim timeline in Texas.

Week 2–6: Estimate Review and Negotiation

After inspections conclude, repair estimates begin circulating between contractors and insurance carriers. Sometimes both sides agree quickly. Sometimes they do not. Common negotiation topics include:

| Claim Issue | Why It Matters |

|---|---|

| Full vs partial replacement | Major cost difference |

| Code upgrades | Compliance expenses |

| Flashing replacement | Water protection concerns |

| Ventilation corrections | System performance |

| Labor pricing | Regional market differences |

Supplement requests often appear during this phase. A supplement is an additional repair cost discovered after deeper inspection or repair work begins. Supplements are extremely common during the hail damage claim timeline in Texas.

Complex Negotiations Often Delay Claims

Insurance negotiations can sometimes resemble an operational anastomosis, where multiple systems and moving parts must connect efficiently for the process to function smoothly. Poor communication between contractors, adjusters, and homeowners often slows approvals significantly.

Week 4–8: Claim Approval or Partial Denial

At this stage, homeowners generally receive one of several outcomes:

- Full approval

- Partial approval

- Request for additional information

- Partial denial

- Full denial

Payment structure also becomes very important here.

Understanding ACV and RCV Payments

Many policies initially pay actual cash value first before releasing recoverable depreciation later. Here is a simplified breakdown:

| Payment Type | Meaning |

|---|---|

| ACV | Depreciated initial payment |

| Deductible | Homeowner out-of-pocket amount |

| Recoverable depreciation | Released after repairs finish |

Many homeowners mistakenly expect one full payment immediately. That rarely happens. Understanding these payment stages helps homeowners better manage the hail damage claim timeline in Texas.

Month 2–4: Roof Repairs or Replacement

Once the claim receives approval, repair scheduling begins. This phase depends heavily on contractor availability. After large storms, roofing schedules fill quickly. Several factors can delay repairs:

- Permit approvals

- Material shortages

- Labor availability

- HOA requirements

- Weather interruptions

Texas weather itself can create additional complications. New storms sometimes hit before repairs are even completed.

Final Payment and Claim Closure

Once repairs finish, final documentation gets submitted. That may include:

- Completion invoices

- Final photos

- Contractor certifications

- Material receipts

The insurance carrier then reviews the documentation before releasing recoverable depreciation. Only after final payment does the hail damage claim timeline in Texas officially conclude.

Common Delays That Slow Down Texas Hail Claims

Not all delays come from insurance carriers. Homeowners unintentionally create many problems themselves.

Waiting Too Long to File

Older hail damage becomes harder to prove over time. Exposure to sun, rain, and wind can gradually alter roof conditions and weaken visible evidence. Fast reporting helps preserve claim credibility.

Contractor Availability Problems

Reputable roofing contractors often become fully booked after major storms. Unfortunately, rushed homeowners sometimes hire inexperienced crews simply to move faster. That can create major workmanship issues later.

Weak Documentation

Claims supported by poor evidence usually move slower. Strong documentation should include:

- Date-stamped photos

- Inspection reports

- Weather verification

- Contractor estimates

- Communication records

Organization matters.

Insurance Disputes

Some delays become unavoidable because disagreements emerge during inspections or estimate reviews. Common disputes include:

- Matching issues

- Scope disagreements

- Code upgrades

- Pricing conflicts

- Cosmetic damage exclusions

Insurance negotiations sometimes involve balancing repair evidence and policy interpretation in ways similar to financial isostasy, where competing pressures gradually seek equilibrium.

Texas Insurance Deadlines Homeowners Should Know

Texas law imposes deadlines on both homeowners and insurance carriers. Understanding them helps avoid preventable claim problems.

Prompt Notice Requirements

Most insurance policies require homeowners to report damage promptly. Delays may allow carriers to argue that damage worsened because repairs or inspections were postponed.

Texas Prompt Payment of Claims Act

Texas law generally requires insurers to:

- Acknowledge claims

- Begin investigations

- Request supporting information

- Issue claim decisions within required timelines

Catastrophe events can complicate scheduling, but insurers still remain subject to legal obligations.

Legal Time Limit Considerations

Homeowners should not ignore unresolved disputes for extended periods. Waiting too long to challenge underpaid or denied claims can limit future legal options.

How Public Adjusters Help Speed Up Hail Claims

Some claims remain straightforward. Others become extremely complex. Public adjusters often help organize and manage difficult claims more efficiently.

Organizing Documentation

Public adjusters help structure claims professionally by organizing:

- Photos

- Inspection reports

- Estimates

- Policy documents

- Communication records

Strong organization often improves claim efficiency dramatically.

Identifying Missed Damage

Experienced claim professionals frequently identify:

- Flashing problems

- Ventilation deficiencies

- Hidden roof impacts

- Code upgrade requirements

- Underestimated repair scope

Those details can materially affect settlement amounts.

Negotiating with Insurance Carriers

Negotiation becomes difficult when homeowners are unfamiliar with roofing systems or policy language. Experienced adjusters understand how to present supporting evidence effectively.

Signs Your Hail Claim Is Stalling

Some delays are normal. Others signal bigger problems.

Repeated Inspection Requests

Multiple reinspections may indicate internal disagreement regarding coverage.

Long Communication Gaps

Weeks without updates often signal claim handling delays. Consistent follow-up matters.

Extremely Low Settlement Offers

Low initial estimates sometimes reflect incomplete scopes rather than final claim value.

Delayed Final Payments

Final depreciation payments should not remain unresolved indefinitely after repairs finish.

Tips to Keep Your Texas Hail Claim Moving Faster

Homeowners can improve claim efficiency significantly by staying proactive.

Stay Organized

Keep all claim-related materials together:

- Emails

- Photos

- Receipts

- Estimates

- Inspection reports

Simple organization prevents major confusion later.

Respond Quickly

Fast responses help keep claims moving smoothly. Delays in communication often create additional bottlenecks.

Keep All Repair Records

Save:

- Contractor invoices

- Material receipts

- Completion photos

- Warranty information

Detailed records protect homeowners long after repairs finish.

Work with Reputable Professionals

Experienced local roofing contractors usually understand Texas storm claims far better than temporary storm-chasing crews. That experience matters during the hail damage claim timeline in Texas.

What Happens If a Hail Claim Gets Denied?

A denial does not always mean the process is over.

Review the Denial Letter Carefully

Understand why the claim was denied. Common reasons include:

- Wear and tear exclusions

- Insufficient evidence

- Prior damage

- Cosmetic damage limitations

Request a Reinspection

Additional inspections sometimes uncover overlooked damage. Especially when stronger documentation becomes available later.

Submit Supplemental Evidence

Additional photos, contractor reports, and weather data may strengthen the claim significantly.

Consider Professional Assistance

Complex disputes often benefit from experienced claim representation, particularly when major roof replacement costs are involved.

Conclusion

The hail damage claim timeline in Texas can move quickly or stretch across several months depending on storm severity, documentation quality, contractor availability, and insurance negotiations. Preparation makes a major difference. Homeowners who document damage early, communicate consistently, stay organized, and understand the claim process usually avoid many of the delays that create frustration later. Texas storms may arrive suddenly. But handling the insurance process carefully and strategically helps homeowners protect both their property and their financial recovery throughout the entire hail damage claim timeline in Texas.

FAQs

Most claims take several weeks to a few months depending on storm severity, inspection schedules, and repair complexity.

Document visible damage, protect the property from further leaks, and schedule a professional roof inspection as soon as possible.

Yes. Insurance carriers may argue the damage resulted from wear, aging, or delayed reporting if too much time passes before filing.

Coverage depends on the policy terms, exclusions, deductible, and whether the damage is considered functional or cosmetic.

Large storm volume, contractor shortages, documentation issues, and claim disputes can all delay the process.

Recoverable depreciation is the withheld portion of a replacement cost claim that is typically released after repairs are completed.

A public adjuster may help when claims become complicated, underpaid, delayed, or disputed.

Yes. Homeowners generally have the right to select the contractor they want for roof repairs or replacement.

You can request a supplement, submit contractor estimates, or seek additional claim review if the scope appears incomplete.

Fast documentation, organized records, quick communication, and working with experienced professionals can help keep the claim moving efficiently.