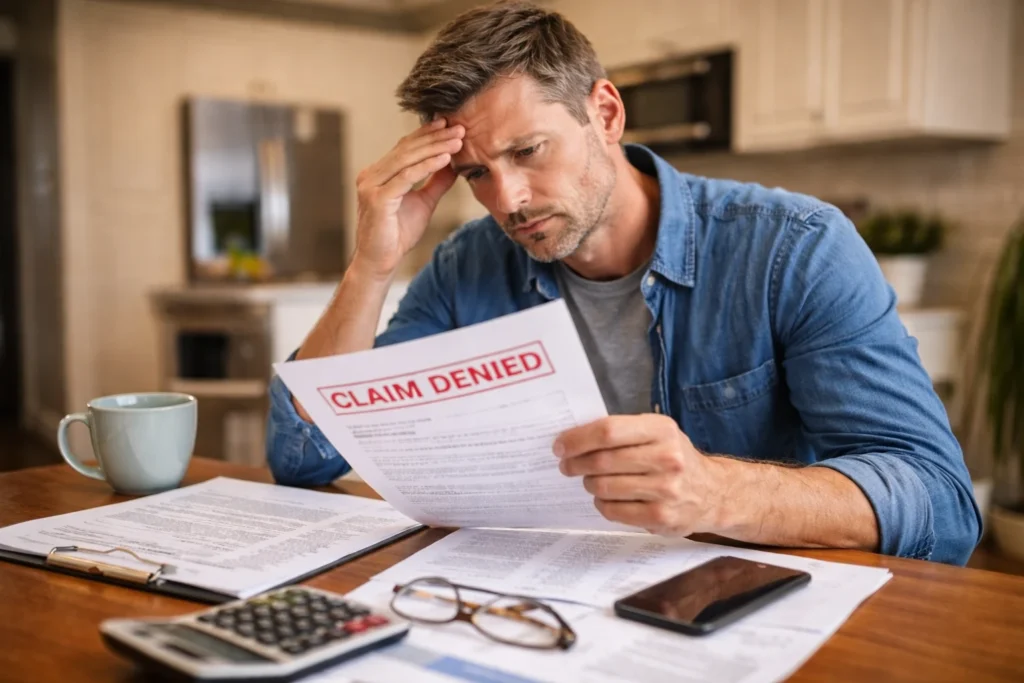

Getting a denial letter after filing a hail claim can feel like a punch to the gut. You expected help. You paid premiums for years. And now, you’re stuck staring at a document that says “no.” If you’re dealing with a hail claim denied in Texas, here’s the truth: this isn’t the end of your claim. Not even close. In many cases, it’s just the beginning of the real process.

I’ve seen it happen over and over. Claims denied. Then reopened. Then approved sometimes for tens of thousands more than the original estimate. The difference? Strategy, documentation, and knowing exactly how to respond. Let’s walk through what actually works.

Why Hail Claims Get Denied in Texas

Before you fight back, you need to understand what you’re up against. Insurance companies don’t randomly deny claims. There’s always a reason. Sometimes it’s valid. Often, it’s questionable.

“No Storm Damage Found”

This is the most common reason behind a hail claim denied in Texas. The adjuster inspects your roof and concludes there’s no hail damage just normal wear and tear. That’s their call. But it’s not always accurate.

Hail damage can be subtle. Especially on:

- Asphalt shingles (look for bruising)

- Metal surfaces (dents on vents, flashing)

- Soft materials (gutters, downspouts)

Miss those signs, and the claim gets denied.

Policy Exclusions and Fine Print

Insurance policies are packed with limitations.

You might run into:

- Cosmetic damage exclusions

- Roof age restrictions

- Actual Cash Value (ACV) policies instead of Replacement Cost Value (RCV)

Late Filing or Weak Documentation

Timing is everything. If you waited too long after the storm or didn’t document the damage properly your claim becomes easier to deny.

Incomplete Inspections

Let’s be honest. Not every inspection is thorough. Some are rushed. Some miss key indicators. Some rely too heavily on surface-level checks. And when that happens, you end up with a denied claim that shouldn’t have been denied.

Step 1 – Carefully Review Your Denial Letter

Don’t skim it. Read it line by line.

What to Look For

- Exact reason for denial

- Policy language cited

- Inspection notes and dates

This is your roadmap. It tells you exactly what the insurance company is relying on.

Red Flags to Watch

- Vague explanations like “no covered damage”

- Heavy use of “wear and tear”

- Lack of specific findings

Step 2 – Get a Professional Roof Inspection

This step changes everything. A second opinion done right can completely shift your claim.

Who Should You Call?

| Professional Type | Role | When to Use |

| Roofing Contractor | Identifies visible damage | First step |

| Public Adjuster | Builds claim + negotiates | Best for disputes |

| Engineer | Provides technical analysis | Complex cases |

Why It Matters

An independent inspection often reveals:

- Missed hail impacts

- Soft metal damage

- Granule loss patterns consistent with hail

And once you have that evidence? You’re no longer arguing. You’re proving.

Step 3 – Document Your Hail Damage Like a Pro

Documentation is leverage. Without it, your case is weak. With it, your claim becomes hard to ignore. If you’re wondering How to Document Hail Damage for an Insurance Claim, the process is more detailed than most homeowners expect and getting it right can be the difference between approval and another denial.

What to Capture

- Close-up photos of roof damage

- Wide shots showing roof slopes

- Dents on gutters, vents, and AC units

- Interior water stains or leaks

Pro Tips

- Use timestamps

- Shoot in good lighting

- Take multiple angles

What Most Homeowners Miss

- Collateral damage (mailboxes, fences)

- Matching issues (new vs old shingles)

- Interior signs that connect to roof damage

This is where claims are won.

Step 4 – Understand Your Policy (ACV vs RCV)

If your hail claim denied in Texas involves payment disputes, this section matters more than you think.

Replacement Cost Value (RCV)

Covers the full cost to replace damaged property (minus deductible).

Actual Cash Value (ACV)

Pays depreciated value. Less money. Sometimes significantly less.

Understanding financial concepts like depreciation and valuation can feel complex almost like navigating topics such as Epistemology, where interpretation plays a major role. Insurance carriers interpret policy language in ways that benefit them, which is exactly why homeowners need clarity.

Why This Matters

Some denials aren’t true denials they’re underpayments disguised as policy limitations. Understanding this difference helps you push back intelligently.

Step 5 – Request a Reinspection

This is your first formal move. And it’s powerful.

How to Do It Right

- Submit new evidence (photos, reports)

- Reference specific damage missed

- Stay factual not emotional

What to Expect

- A different adjuster may be assigned

- You can walk them through the damage

- Outcomes often change with better documentation

Many hail claim denied in Texas cases get approved at this stage.

Step 6 – File a Formal Dispute or Appeal

If reinspection doesn’t resolve it, escalate.

What Your Dispute Should Include

- Clear statement of disagreement

- Supporting documentation

- Contractor or adjuster reports

- Weather data showing hail event

Step 7 – Hire a Public Adjuster (Game Changer)

This is where things shift. A public adjuster works for you not the insurance company.

What They Actually Do

- Review your policy in detail

- Document damage thoroughly

- Handle all communication

- Negotiate for maximum payout

For many homeowners dealing with a hail claim denied in Texas, this is the turning point.

Step 8 – Consider Legal Options (If Necessary)

Sometimes, escalation is unavoidable.

When to Call an Attorney

- Repeated denials without valid reasoning

- Evidence clearly supports your claim

Final Thoughts: Don’t Accept “Denied” as the Final Answer

A hail claim denied in Texas feels final. It’s not. It’s a position. One you can challenge. Take action. Get a second opinion. Document everything. Bring in help if needed. Because the homeowners who push back? They’re the ones who get paid.

FAQs

Yes, you can reopen a claim if you have new evidence such as photos, inspection reports, or contractor estimates that support storm damage.

Most policies allow disputes within a specific timeframe, often up to one year from the date of loss, but you should act as quickly as possible.

Insurance companies may argue the damage is due to wear and tear, poor maintenance, or not severe enough to qualify under your policy.

Absolutely. A professional inspection can uncover missed damage and provide the evidence needed to challenge the denial.

Clear photos, video documentation, contractor reports, and weather data confirming a hail event are the strongest forms of proof.

Filing a dispute itself typically does not increase premiums, but multiple claims in a short period could impact your policy rates.

Yes, a public adjuster represents your interests, documents damage thoroughly, and negotiates with the insurance company to improve your outcome.

Yes, older roofs can still qualify if hail damage is present, though the payout may be based on depreciation under an ACV policy.

It can take anywhere from a few weeks to a couple of months depending on the complexity of the dispute and responsiveness of the insurer.

In many cases, yes especially if the damage is significant, since successful disputes can result in thousands of dollars in additional coverage.