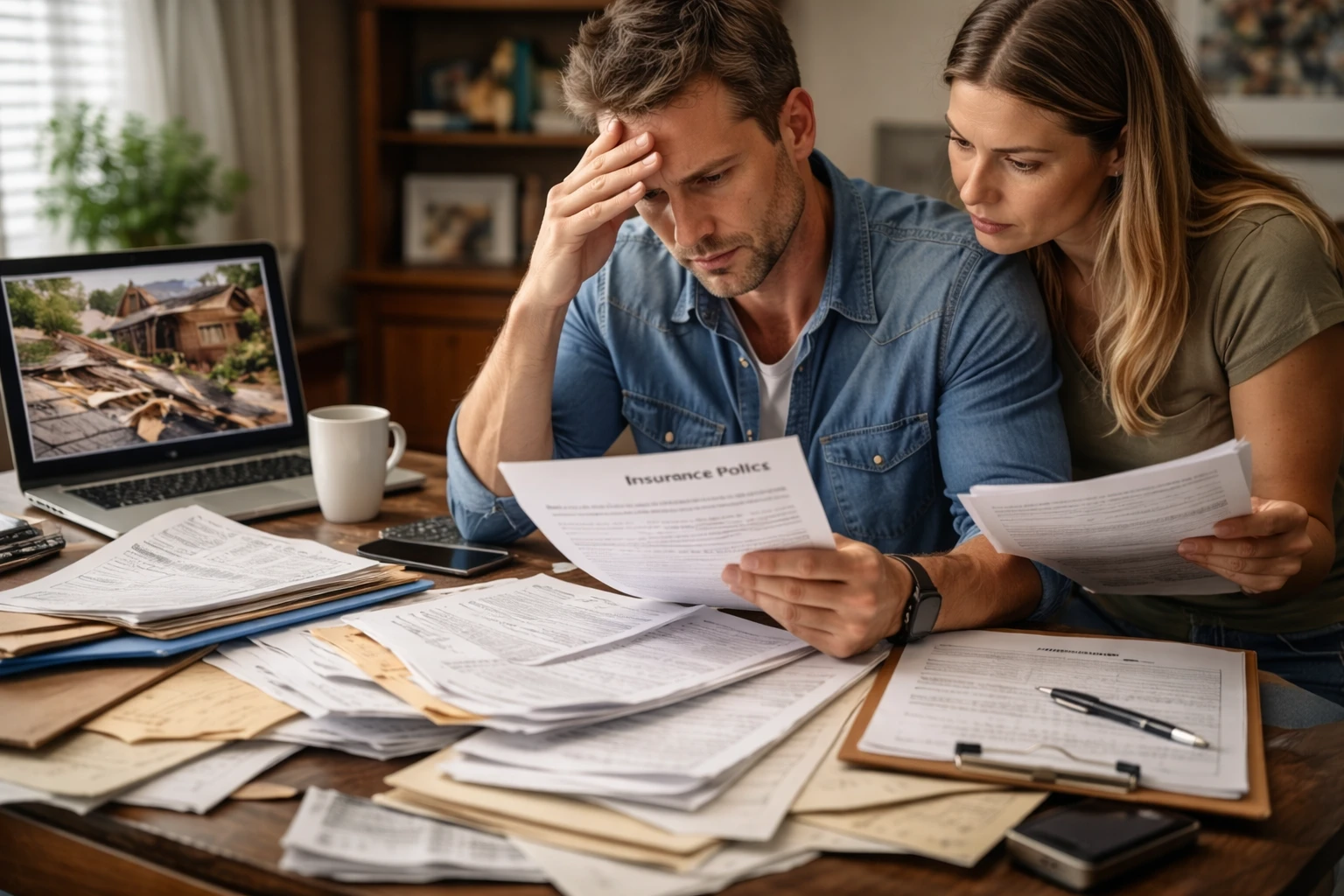

Property damage is never convenient. A storm tears through your roof, a pipe bursts overnight, or a fire leaves part of your home unlivable. In those stressful moments, most homeowners immediately contact their insurance company. That is the standard first step. But there is another important question that often gets overlooked: when to call a public adjuster.

Understanding when to call a public adjuster can make a real difference in how smoothly your claim proceeds and how fair the final settlement is. Insurance claims are not always straightforward. Policies contain detailed language, damage assessments can be complex, and settlement negotiations may become difficult. That is where a public adjuster can step in.

In this guide, we will break down exactly when to call a public adjuster, what they do, and how they can help homeowners and business owners navigate complicated insurance claims.

What Is a Public Adjuster?

Before discussing when to call a public adjuster, it helps to understand what a public adjuster actually does.

A public adjuster is a licensed professional who represents policyholders during insurance claims. Unlike adjusters employed by insurance companies, public adjusters work exclusively on behalf of the property owner.

They evaluate damage, review policies, prepare claim documentation, and negotiate with the insurer to help ensure the claim reflects the full scope of the loss.

Types of Adjusters in an Insurance Claim

Not all adjusters serve the same role. The insurance industry typically involves three types:

| Adjuster Type | Who They Work For | Role |

| Company Adjuster | Insurance company | Investigates claims for the insurer |

| Independent Adjuster | Contracted by insurance company | Handles claims on behalf of insurers |

| Public Adjuster | Policyholder | Represents the homeowner or business owner |

The key difference is simple. Public adjusters work for you, not the insurance company.

Why Insurance Claims Can Become Complicated

Many homeowners assume the claims process is simple. File a claim, get paid, and repair the damage.

In reality, things rarely move that smoothly.

Insurance policies are complex legal documents. Coverage limits, exclusions, depreciation rules, and policy conditions all influence what is paid and what is not.

Even something as straightforward as roof damage can involve multiple assessments:

- Structural damage

- Interior water damage

- Insulation damage

- Mold risk

- Personal property loss

Each detail affects the final settlement.

For homeowners who are already dealing with repairs, temporary housing, and family disruptions, managing a complicated claim can quickly become overwhelming.

That is why understanding when to call a public adjuster matters.

When to Call a Public Adjuster

Some claims can be handled easily without professional assistance. Others benefit greatly from expert representation.

Here are the situations where knowing when to call a public adjuster becomes critical.

After Major Property Damage

Large losses are one of the most common reasons homeowners seek help.

Examples include:

- House fires

- Severe storm damage

- Hurricane destruction

- Tornado impacts

- Major flooding

- Structural collapse

These events typically involve extensive inspections, detailed repair estimates, and multiple rounds of negotiation with insurers.

A public adjuster helps ensure that all damages are documented properly and that nothing is overlooked.

Large claims also involve large financial stakes. Even small differences in damage estimates can change settlement amounts significantly.

When Your Claim Is Denied

Insurance claim denials happen more often than many people expect.

A denial may occur because:

- The insurer believes the damage is not covered

- The claim lacks sufficient documentation

- The damage is attributed to maintenance issues

- The insurer disputes the cause of loss

When this happens, homeowners often feel stuck.

This is one of the clearest moments when to call a public adjuster.

A public adjuster can review the policy, examine the denial, and determine whether coverage was incorrectly denied. In some cases, additional documentation or a revised claim presentation can reopen the case.

When the Settlement Offer Seems Too Low

Another common scenario involves underpaid claims.

The insurance company sends a payment. It may look reasonable at first glance. But when contractors provide repair estimates, the numbers do not match.

This gap is surprisingly common.

Public adjusters evaluate the full scope of damage and prepare detailed estimates to support a higher settlement.

Signs a settlement may be too low include:

- Repair estimates exceed the claim payment

- Important damage areas were not inspected

- Interior damage was overlooked

- Materials listed in the estimate are lower quality than what existed

If you are questioning the settlement amount, that may be exactly when to call a public adjuster.

When the Claims Process Becomes Overwhelming

After property damage, life becomes chaotic.

You may be juggling:

- Temporary housing

- Contractor meetings

- Insurance inspections

- Property inventories

- Paperwork submissions

It is a lot.

Public adjusters handle many of these responsibilities. They organize documentation, communicate with the insurance company, and track claim progress.

For many homeowners, the benefit is simple: less stress and more clarity.

When Damage Is Difficult to Document

Not all damage is immediately visible.

Some of the most expensive property damage hides behind walls, inside ceilings, or within structural systems.

Examples include:

- Hidden water damage

- Smoke contamination

- Electrical damage

- Structural weakening

- Mold growth

These losses require careful documentation.

Public adjusters often work with contractors, engineers, and restoration specialists to ensure all damages are identified and included in the claim.

When the Claim Is Large or Complex

Some claims involve more than a single structure or repair.

Complex claims may include:

- Multiple buildings

- Detached structures

- Extensive personal property loss

- Business interruption

- Equipment damage

In commercial claims, the stakes become even higher.

For business owners, delayed or insufficient claims can disrupt operations for months.

In these situations, knowing when to call a public adjuster can significantly affect financial recovery.

Types of Damage That Often Require Public Adjusters

Certain property damage scenarios consistently lead to complicated claims.

Storm and Hurricane Damage

Severe weather often creates multiple layers of damage:

- Roof failure

- Water intrusion

- Structural shifts

- Electrical damage

- Debris impact

These claims may require coordination between roofing contractors, structural engineers, and restoration professionals.

Fire and Smoke Damage

Fire claims rarely involve just burned materials.

Additional damage can include:

- Smoke contamination

- Soot damage

- Water damage from firefighting

- Structural instability

- HVAC contamination

Public adjusters help ensure these secondary damages are properly included.

Water Damage

Water losses can escalate quickly.

Common sources include:

- Burst pipes

- Appliance failures

- Roof leaks

- Sewer backups

- Plumbing issues

Water damage also increases the risk of mold growth, which may introduce additional coverage questions.

Commercial Property Losses

Business owners face additional complications such as:

- Lost income

- Equipment replacement

- Inventory damage

- Operational downtime

These claims often involve extensive financial documentation.

Signs You Should Contact a Public Adjuster Immediately

Sometimes the need for help becomes obvious.

Watch for these warning signs:

- Insurance communication becomes slow or inconsistent

- The insurer requests excessive documentation

- Damage inspections feel incomplete

- Settlement offers arrive quickly and seem unusually low

- You feel pressured to accept a payment

These signals often indicate that professional representation could help.

Recognizing these moments helps homeowners decide when to call a public adjuster before problems escalate.

Benefits of Hiring a Public Adjuster

Hiring a public adjuster provides several advantages.

Improved Claim Documentation

Thorough documentation strengthens claims. Public adjusters prepare detailed reports, photos, and estimates to support the claim.

Professional Negotiation

Insurance negotiations can be technical. Public adjusters understand claim valuation and policy interpretation.

Reduced Stress

Claims can take weeks or months. Having a professional manage the process allows homeowners to focus on recovery.

Potentially Higher Settlements

Because public adjusters evaluate the full scope of damage, claims may reflect more accurate repair costs.

When You Might Not Need a Public Adjuster

Public adjusters are valuable, but they are not necessary for every claim.

You may not need one if:

- Damage is minor

- The insurance company responds quickly

- The settlement fully covers repair costs

- The claim process remains straightforward

Small claims are often resolved quickly without complications.

The key is recognizing the difference between simple claims and complex losses.

How the Public Adjuster Process Works

For homeowners wondering when to call a public adjuster, it also helps to understand the typical process.

Step 1: Initial Consultation

The public adjuster reviews the property damage and insurance policy.

This step determines whether professional assistance is necessary.

Step 2: Damage Documentation

Next comes a detailed inspection.

This may include:

- Photographs

- Repair estimates

- Structural evaluations

- Property inventories

Step 3: Claim Preparation

All documentation is organized into a claim package submitted to the insurer.

Step 4: Negotiation

The public adjuster communicates directly with the insurance company to negotiate the settlement.

This stage may involve multiple discussions, inspections, and revised estimates.

How to Choose the Right Public Adjuster in Texas

Choosing the right professional matters.

Here are several factors to consider.

Verify Licensing

Public adjusters must be licensed by the state. Always confirm credentials before hiring.

Look for Relevant Experience

Property claims vary widely.

Experience with specific damage types—such as fire or storm damage—can be valuable.

Understand Fee Structures

Public adjusters typically work on a contingency fee.

This means they receive a percentage of the claim settlement rather than charging upfront fees.

Check Reputation

Reviews, testimonials, and professional references provide insight into past client experiences.

Understanding Insurance Claims and Policyholder Rights

Insurance claims operate within a regulated framework designed to protect policyholders.

For example, federal guidance related to disaster assistance and recovery can be found through the Federal Emergency Management Agency (FEMA)

These resources explain how disaster recovery programs interact with insurance claims and homeowner responsibilities.

Understanding these frameworks can help property owners navigate the claims process more confidently.

Final Thoughts: Knowing When to Call a Public Adjuster

Property damage is stressful. There is no way around it.

When disaster strikes, homeowners suddenly find themselves managing repairs, contractors, paperwork, and insurance negotiations all at once. It is a lot to handle.

This is why understanding when to call a public adjuster can make such a difference.

The right timing can help:

- Improve claim documentation

- Reduce stress during recovery

- Ensure damage is fully evaluated

- Support fair settlement negotiations

Not every claim requires professional assistance. But when losses are large, complicated, or disputed, bringing in a public adjuster can be one of the smartest decisions a property owner makes.

If you ever find yourself facing a difficult claim, remember this simple rule: when the claim becomes complex, overwhelming, or uncertain, that may be exactly when to call a public adjuster.

FAQs

A public adjuster represents the policyholder during an insurance claim by evaluating damage, preparing documentation, and negotiating with the insurance company for a fair settlement.

You should consider calling a public adjuster as soon as you notice significant damage, especially if the claim is large, complicated, or difficult to document.

No, public adjusters work exclusively for the policyholder and advocate for the homeowner or business owner during the claim process.

Most public adjusters work on a contingency basis, meaning they receive a percentage of the final insurance settlement rather than charging upfront fees.

Yes, a public adjuster can review the denial, examine the insurance policy, and help reopen or appeal the claim if coverage was incorrectly rejected.

For minor damage or straightforward claims, you may not need one, but they are often helpful for large or complex losses.

Yes, public adjusters must be licensed and regulated by the state, ensuring they meet professional and legal requirements.

In many cases, a public adjuster can actually streamline the process by organizing documentation and communicating directly with the insurance company.

Major storm damage, fire damage, water damage, and large commercial losses are situations where public adjusters are frequently involved.

Yes, homeowners can hire a public adjuster at almost any stage of the claims process, including after filing the initial claim or receiving a settlement offer.